What Is the Snowball Method?

How Does It Work?

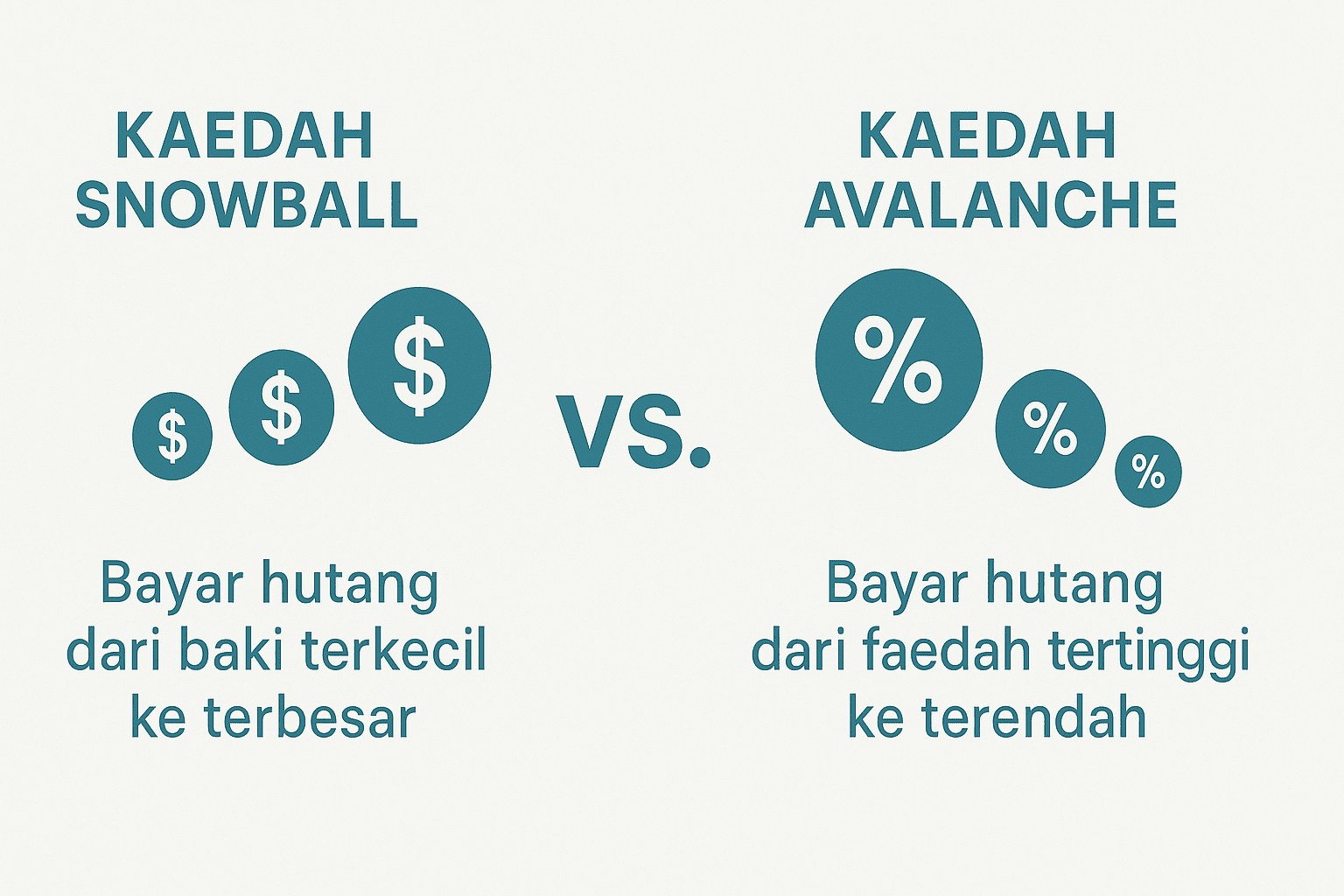

The Snowball method begins by listing all your debts in order from the smallest to the largest amount. You continue paying the minimum instalments for every debt except the smallest one. Any extra money you have each month should go toward settling the smallest debt as quickly as possible. Once that debt is cleared, you move on to the next using the same approach. Repeat this process until all your debts are paid off.

Advantages of the Snowball Method

This method offers a sense of satisfaction as small debts are paid off quickly, which helps to boost motivation and keeps you going. It is suitable for those who need psychological encouragement to stay disciplined in managing their debt payments.

Disadvantages of the Snowball Method

Although effective, the Snowball method may lead to higher interest costs over time since it does not prioritise debts with high interest rates. In terms of total repayment, it is less efficient than the Avalanche method, which focuses more on interest savings.

What Is the Avalanche Method?

The Avalanche method, also known as the debt avalanche technique, focuses on repaying high-interest debts first, regardless of the remaining balance.

How Does It Work?

The Avalanche method begins by listing all your debts in order from the highest to the lowest interest rate. You continue paying the minimum instalments for all debts except the one with the highest interest rate. Any extra funds should be channeled toward that high-interest debt until it’s fully repaid. Once cleared, redirect the extra payments to the debt with the next highest interest rate. Repeat this process until all your debts are paid off.

Advantages of the Avalanche Method

Disadvantages of the Avalanche Method

However, the Avalanche method may feel slow at first because smaller debts are not cleared quickly. It may not be suitable for those who need early progress to stay motivated, unlike the Snowball method which provides quicker wins through small debt repayments.

Snowball vs. Avalanche: Which Is Better?

The Avalanche method, on the other hand, is better suited for those who want to minimise interest costs by tackling high-interest debts first. It’s more efficient from a mathematical standpoint but requires more patience.

- Debt A: RM2,000 (18% interest)

- Debt B: RM6,000 (12% interest)

- Debt C: RM8,000 (8% interest)

Can You Combine Both Methods?

Choose the Right Method Based on Your Situation